In this new edition of the Altman-Z Score of PV Module Manufacturers, we rank a dozen leading PV module manufacturers according to their financial strength.

The report answers the questions:

Which PV module manufacturers are financially strong? and which manufacturers are in the risk zone of going bankrupt within the coming 2 years?

Edition 1, 2017: how do PV module manufacturers rate on the Altman Z-score?

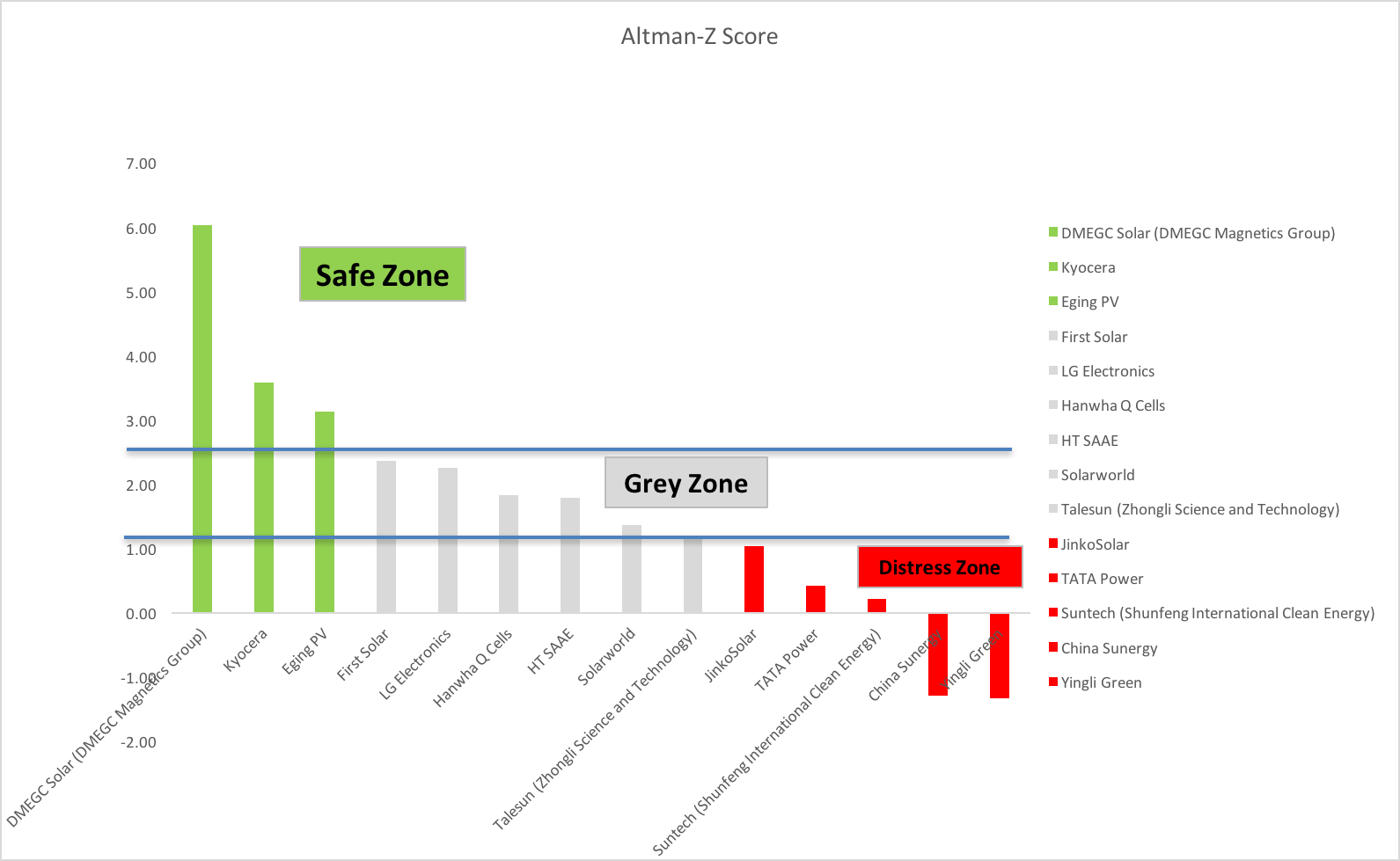

The following table shows the Altman Z-Scores of major, publicly listed Asian, European and American manufacturers in the current Q1 2017:

Altman Z-Scores – Edition 1, 2017 (Source: gurufocus.com)

Click on the graph to enlarge:

Continuing the trend of our previous Altman Z-Score analysis from the end of September 2016, emerging Chinese manufacturer DMEGC Solar Energy defends its No. 1 position in the chart with a very healthy score of 6.03. The vertically integrated producer of polysilicon, wafers, cells and modules is thus far ahead of PV industry heavyweights such as LG, First Solar, and Solarworld.

The Altman Z-Score of Hanwha Q-Cells continues its upward trend with 1.84 (up from 1.67 in September 2016 and 0.86 in March 2016), mirroring the improving financials of the once crippling Q-Cells.

While DMEGC again leads in the top position in our Altman Z-Score, Yingli Green continues to rank in the bottom area of the Distress Zone which means it’s likely to face bankruptcy within the next 2 years. China Sunergy (CSUN) continues its downward trend with a score of -1.29 (down from previously -0.46 in September 2016 and -0.45 in March 2016), ranking it now close to Yingli.

How to interpret companies in the ‘Grey Zone’?

With a large number of companies in the ‘Grey Zone’, how to interpret these scores when selecting a manufacturer?

While ideally, a manufacturer is in the ‘Green Zone’, some companies have been consistently in the Grey Zone for years.

Take for instance HT SAAE. Here are a number of Altman Z-Scores over the years:

2.28 on Dec ’13

1.75 on Dec ’14

1.88 on Dec ’15

Currently stands at 1.80 (3 Feb ’17)

These numbers show HT SAAE has been stable for years. Add the fact that HT SAAE is a state-owned company under China Aerospace Science and Technology Corporation, and they may just as well be one of the most solid companies on the list.

For those unfamiliar with the Altman-Z Score, here’s an introduction:

What is the Altman Z-score?

The Altman Z-score is a formula to predict bankruptcy. This formula is used to predict corporate defaults and the status of financial distress. The formula uses the factors profitability, liquidity, leverage, activity, and solvency to predict if a firm will go into bankruptcy within two years.

As the Altman Z-score was originally designed to assess public manufacturing companies with assets of more than USD 1 million, this formula is an excellent way to assess which PV module manufacturers may be in trouble within the next 2 years.

The formula is nowadays widely accepted by auditors, accountants, courts, and database systems used to evaluate loans.

The formula dates from the 1960s and was published by Edward L. Altman, who back then was working as an Assistant Professor of Finance at New York University.

Altman Z-score: how likely is a PV module manufacturer to go bankrupt within the next 2 years?

How reliable is the Altman Z-score formula?

The Altman-Z Score isn’t perfect, however, we’d say it’s reliable enough to make a proper judgment on the financial situation of a PV module manufacturer:

Between 1968 and 1999 the formula has been put to the test multiple times. The model was found to be about 80-90% accurate in predicting bankruptcy one year before the event (with a Type II error, classifying the firm as bankrupt when it does not go bankrupt of approximately 15%–20%*).

(*Source: pages.stern.nyu.edu/~ealtman/Zscores.pdf)

How’s the Altman Z-score calculated?

Altman Z-Score formula = 1.2A + 1.4B + 3.3C + 0.6D + 1.0E

The original formula is broken down as follows:

A = Working Capital/Total Assets: measures liquid assets in relation to the size of the company

B = Retained Earnings/Total Assets: measures profitability that reflects the company’s age and earning power

C = Earnings Before Interest & Tax/Total Assets: measures operating efficiency apart from tax and leveraging factors. It recognizes operating earnings as being important to the long-term viability

D = Market Value of Equity/Total Liabilities: adds a market dimension that can show up security price fluctuation as a possible red flag

E = Sales/Total Assets: standard measure for total asset turnover

How is the Altman Z-scores interpreted?

The scores are categorized into 3 zones called the Safe Zone, Grey Zone and Distress Zone:

Safe Zone = Z > 2.6

Grey Zone = 1.1 < Z < 2.6

Distress Zone = Z < 1.1 –

What happens to solar module warranties when a manufacturer goes bankrupt?

When a PV manufacturer goes bankrupt, its product- and performance warranties will no longer be valid. Valid warranties are important for PV plant developers and PV project owners who want to safeguard their project ROIs. A product warranty is important to cover defects related to the solar module’s workmanship while a performance warranty is important to have in place in case solar module’s degrade faster than anticipated and their output is lower than expected.

One solution to eliminate bankruptcy risk is to purchase a solar module warranty insurance, such as the Solarif warranty insurance. Another solution is to make 100% sure that you’re purchasing a quality solar module. Sinovoltaics is a specialized company that can help to safeguard the quality of your solar components.

Altman Z-Score and limiting real-world factors

In our first Altman Z-Score article we already outlined that while the Altman Z-Score is quite reliable to make proper judgments on the financial shape of a PV manufacturer, there are of course many more local factors that can come into play in the wake or aftermath of a bankruptcy of a manufacturer.

Such factors can be of strategic importance for a manufacturer, the number of people employed, unique technologies or intellectual properties, shareholder interests, and so on.

Exemplifying the case of China (but also of course applicable to other countries), companies with strategic importance to (local) governments, are likely to enjoy some degree of support when filing for bankruptcy.

Do you want access to Altman Z-Scores of all leading PV module manufacturers? Access Full Version: Altman-Z Report with 60+ PV module manufacturers for FREE.

Anony

on 22 Feb 2022Anonymous

on 13 Feb 2017