After years of relentless price declines, the global solar industry is entering a new phase. PV module prices are rising again and this time, the shift appears more structural than temporary.

In Sinovoltaics’ webinar #36 featuring Marius Mordal Bakke, Vice President and Head of Solar & Storage Research at Rystad Energy, industry experts unpacked the key forces driving higher module prices in 2026. While China’s removal of export tax rebates for solar products has captured headlines, the discussion revealed a far more complex picture involving silver shortages, polysilicon market dynamics, oversupply pressures, and changing project economics across Europe.

The webinar explored how rising manufacturing costs are reshaping global procurement strategies, why silver has become one of the industry’s most critical cost drivers, and how battery storage is increasingly essential for maintaining solar project profitability in mature markets.

As developers, EPCs, investors, and procurement teams navigate this evolving landscape, understanding the underlying drivers behind today’s pricing environment has never been more important.

Webinar Transcription

00:00:15

Rasa Jakaitis:

Hello everyone, and a warm welcome to Sinovoltaics’ exclusive webinar.

My name is Rasa Jakaitis, Media Manager at Sinovoltaics, and today I will be moderating this timely webinar on China’s solar export tax rebate removal.

We have witnessed PV module prices rising again, and this time it is not just a short-term fluctuation. After hitting record lows earlier in the cycle, prices started moving up in late 2025. As we enter 2026, that increase is accelerating.

Production cuts, higher import costs, recovering global demand, and major policy changes in China are all contributing to rising prices.

One development stands out in recent headlines: China’s removal of export tax rebates for solar products effective April 1st. This is not merely a policy adjustment, it is a structural shift.

Costs that were previously absorbed within China’s manufacturing system are now being passed down the supply chain. As a result, global pricing, procurement strategies, and project economics are changing.

Today, we will cut through the noise to explain what is really driving PV module prices higher. We will break down the true cost structure of Chinese PV manufacturing, explain how export tax changes affect margins and supplier behavior, and discuss what this means for module availability and project viability worldwide.

Before I introduce our guest speaker, a few quick notes:

- This webinar will last approximately one hour.

- The presentation will be followed by a Q&A session.

- On the right-hand side of your screen, you will see a Q&A chat box. Please use it to submit your questions at any time during the presentation.

- This webinar is being recorded and will be uploaded to Sinovoltaics’ YouTube channel.

If you would like to stay informed about the latest renewable energy developments, please subscribe to our YouTube channel.

Now let me introduce today’s guest speaker.

We are delighted to welcome Marius Mordal Bakke, Vice President and Head of Solar and Storage Research at Rystad Energy.

Marius’ work spans manufacturing trends, supply chain dynamics, and technology competitiveness across the clean energy value chain. At Rystad Energy, he oversees a research team focused on solar and storage deployment forecasts, global manufacturing capacity, supply-demand modeling, and industrial policy impacts.

A few words about myself as I will be moderating this session today.

Over nearly 10 years of professional experience, I have worked in communications roles across multiple international industries, including consumer electronics, medical devices, insurance, and now renewable energy.

For almost four years, I lived in Brussels, in the heart of Europe, before returning to my homeland Lithuania to continue my professional path. At Sinovoltaics, I manage this exclusive webinar program and oversee PR initiatives.

Before handing over the virtual microphone to Marius, let me briefly introduce Sinovoltaics for those joining our webinar program for the first time.

Sinovoltaics is a global technical advisory firm specializing in solar and energy storage projects. We help developers, investors, and manufacturers reduce technical risks through due diligence, quality assurance, and safety assessments.

Our mission is to make renewable energy projects safer, more reliable, and more bankable.

Now I invite Marius to begin his presentation.

Please continue submitting your questions in the Q&A chat box throughout the session.

Marius, the floor is yours.

00:05:02

Marius Mordal Bakke:

Perfect, thank you.

Today we will discuss PV pricing trends and market developments. We can broadly divide this discussion into two parts:

1. Silicon-driven cost increases and their impact on module pricing

2. Cost increases outside the silicon supply chain, particularly silver, which has been the main market driver over the last six months

Before we move into those topics, however, it is important to discuss demand for Chinese modules.

2025 was a major year for module deployments worldwide and also for demand for Chinese modules. However, we expect a decline in annual installations in 2026, largely driven by a slowdown in the Chinese domestic market.

At the same time, we are seeing slower growth in more mature and saturated markets such as Europe and Australia. Historically, these have been key destinations for Chinese modules.

Despite continued global installation growth beyond 2026 — driven primarily by the Middle East, Africa, Southeast Asia, and South Asia — access to these markets is not guaranteed for Chinese manufacturers.

For example:

- Turkey is becoming less accessible to Chinese manufacturers.

- India has imposed restrictions through domestic manufacturing policies.

- The US market has effectively remained inaccessible for years.

Therefore, even if global solar installations continue to rise, demand specifically for Chinese modules is not necessarily expected to increase.

That is an important backdrop before discussing the rest of the market dynamics.

00:07:37

Let us begin with silicon-driven cost increases.

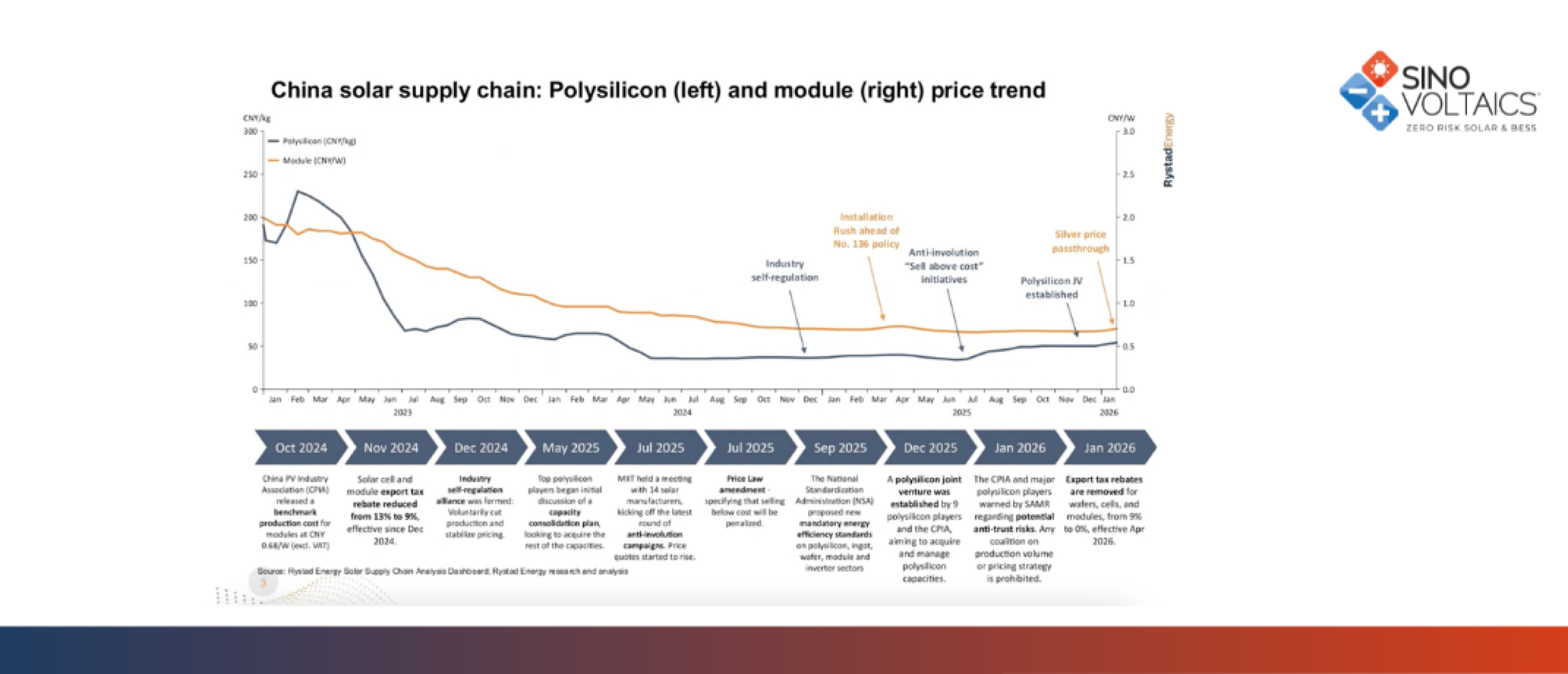

A great deal has happened within the polysilicon market since the supply crunch of 2022, which extended into 2023 and resulted in extremely elevated polysilicon prices.

Naturally, those costs translated throughout the value chain — into wafers, cells, and eventually modules.

Whenever there is movement in polysilicon pricing, there is always a delay before the effects are fully reflected in module pricing.

For example, the rapid decline in polysilicon pricing during 2023 took time before module prices also reached their floor.

As modules reached those historic lows, manufacturers began reporting significant financial losses. Many companies were effectively losing money on every module they produced.

As a result, we began to see attempts at industry self-regulation, including:

- Benchmark production cost agreements established around October 2024

- Industry self-regulation alliances

- Anti-involution campaigns intended to stabilize pricing

However, for a long time, these initiatives had limited effect.

The only meaningful price increase from 2024 into 2025 came from the installation rush ahead of China’s new renewable energy market policies.

Roughly 75% of China’s annual solar installations in 2025 were deployed ahead of June 1st. Naturally, this created a surge in procurement activity and temporarily allowed manufacturers to raise prices.

After that initial demand spike, however, module prices resumed their downward trajectory.

We observed similar dynamics in polysilicon pricing until anti-involution measures and price law amendments introduced in July 2025 helped push polysilicon prices upward.

Still, only a limited portion of those increased costs could be passed through to modules due to persistent oversupply in the market.

Now, however, we are beginning to see domestic Chinese prices increase because of silver cost pass-through.

Manufacturing costs are rising not only because polysilicon prices increased, but also because silver prices moved sharply upward, significantly increasing cell production costs.

As a result, there is now a new cost floor in the market that manufacturers are attempting to reflect through higher module pricing.

The removal of export tax rebates has also supported overseas demand and strengthened manufacturers’ ability to raise prices.

00:10:16

Something important also happened in January this year regarding polysilicon.

Antitrust concerns emerged surrounding self-regulation efforts and proposed joint venture structures.

While gross profit margins improved following anti-involution campaigns, future polysilicon prices began facing downward pressure once concerns about industry consolidation intensified.

The proposed joint venture structure was effectively halted, creating uncertainty around future consolidation strategies.

At current price levels, polysilicon manufacturers are still generating profits, which means there is still room for prices to decline.

This downward pressure on polysilicon could eventually help reduce module production costs further down the line.

If we examine production and inventory trends among polysilicon manufacturers:

- Production began increasing significantly around July 2025.

- At the same time, inventories started declining because downstream manufacturers were stockpiling polysilicon in anticipation of higher prices.

Once manufacturers began generating profits again, the natural response was to increase production.

However, actual transaction volumes did not increase proportionally.

As a result, inventories began accumulating once again.

We are now seeing polysilicon production begin to taper off. Tongwei, the world’s largest polysilicon manufacturer, has already stated its intention to limit production until May 2026 in an effort to stabilize prices.

Nevertheless, significant downward pressure on polysilicon pricing remains.

00:12:48

Now let us move to silver.

While silicon-driven price increases did not fully translate into higher module prices, silver is a different story.

The cost impact from silver has been far greater than silicon-related cost increases.

Silver has been in global undersupply since 2021.

One major issue is that only slightly more than 20% of global silver mines are dedicated silver mines.

Most silver production is actually a byproduct of mining for:

- Zinc

- Copper

- Other industrial metals

This means silver supply is relatively inflexible. If demand spikes, production cannot quickly scale up to match it.

As a result, prices become highly volatile.

This persistent undersupply combined with growing demand caused silver prices to rise sharply throughout the second half of 2025.

Naturally, this translated into significantly higher silver paste prices.

By January 2026, silver paste represented approximately 24–25% of the total module manufacturing cost structure.

At the cell level, silver paste now accounts for nearly half of the cost of a finished solar cell.

This means silver is now one of the most important drivers of future module costs.

00:15:30

If we look specifically at cell manufacturing economics, the picture differs from polysilicon.

Polysilicon manufacturers benefited from improved margins because their costs remained relatively stable while prices increased.

Cell manufacturers, however, experienced rising prices alongside sharply rising costs.

As a result, many cell manufacturers are still not making money despite higher transaction prices.

This is why prices are not expected to decline significantly in the near term.

There is now strong upward price pressure simply because manufacturers are still producing at a loss.

Silver remains the primary driver of margin pressure.

Once silver paste prices accelerated in October 2025, production costs increased substantially, leading to reduced production levels among cell manufacturers.

At the same time, inventories also started falling because overseas demand surged ahead of the removal of export tax rebates.

Module manufacturers raised their quotations significantly, and actual transaction prices rose well above mid-2025 levels.

Importantly, these higher prices were accepted by the market.

Therefore, there is now genuine support for both:

- Higher cell costs

- Higher module prices

The key question moving into 2026 is where costs eventually stabilize.

Silver prices are not necessarily expected to continue rising throughout the entire year.

Many analysts believe silver is currently overpriced.

At the same time, manufacturers are rapidly shifting toward:

- Copper substitution

- High-copper concentration pastes

- Reduced silver usage

Therefore, future module costs will largely depend on:

- The speed of copper adoption

- Whether silver prices remain elevated or normalize

00:18:03

Turning specifically to Europe, the outlook for demand is not particularly strong.

The market is likely to remain oversupplied with Chinese modules for quite some time.

At the same time, access to European demand is becoming more restricted due to:

- Net Zero Industry Act requirements

- Resilience criteria

- European manufacturing support policies

For example, one of Italy’s recent FERX auctions — representing approximately 1 GW of demand — prohibited the use of Chinese solar cells, modules, and inverters.

So while European demand itself may slow, the portion accessible to Chinese manufacturers is shrinking even faster.

The removal of export tax rebates has already triggered a surge in procurement activity across Europe.

However, this trend actually began during the second half of 2025 as companies anticipated the policy change.

As procurement accelerates ahead of the April 1st deadline, we are likely to enter a new market phase afterward where procurement slows significantly.

Whether the market ultimately accepts these elevated prices will depend heavily on future cost dynamics.

00:20:40

Now let us examine how these developments affect solar project economics in Europe.

Throughout 2024 and 2025, merchant solar projects in major European markets such as:

- Germany

- France

- Spain

have experienced deteriorating profitability due to:

- Increasing negative-price hours

- Depressed capture rates

The cumulative number of negative-price hours has steadily increased year over year.

More importantly, these negative-price periods increasingly occur during summer daytime hours — exactly when solar generation peaks.

Because European power markets are heavily interconnected, solar deployment in one country affects neighboring markets as well.

For example, rapid solar expansion in Germany impacts capture prices in:

- Sweden

- Denmark

- Norway

- Other interconnected regions

Although trends are broadly similar across Europe, some markets are more vulnerable to solar cannibalization effects.

Italy, for example, remains a large solar market supported by auctions.

Its average capture rate declined from approximately 85% in Q2–Q3 2024 to around 81% during the same period in 2025.

Germany experienced a far steeper decline — from 56% to 46%.

Spain dropped to approximately 42%.

That means solar projects in Spain were receiving only 42% of the average market price for their generated electricity.

Under merchant exposure, this becomes extremely challenging economically.

As a result, standalone solar projects increasingly depend on:

- Contracts for Difference (CfDs)

- Corporate PPAs

- Hybridization with battery storage

Battery storage is rapidly becoming the key growth enabler for European solar.

Being able to shift electricity generation from negative-price daytime hours into evening peak periods is essential for maintaining project economics.

00:23:47

If we examine Germany more closely, capture rates have declined consistently year after year.

In June 2025, Germany’s capture rate dropped to just 31.5%.

There was some temporary relief in July due to:

- Heatwaves across Europe

- Increased air-conditioning demand

- Weak wind generation

- Limited output from coal and nuclear

However, after those short-term conditions passed, capture rates declined once again.

Italy presents a somewhat different picture.

Unlike Germany, Italy experienced slower solar deployment during the 2010s and only accelerated installations in recent years.

Italy also benefits from market policies that generally prevent electricity prices from falling below zero during solar peak hours.

This provides some protection to solar project economics.

00:26:17

So what does all of this ultimately mean?

It does not mean that Europe is no longer accessible for Chinese module manufacturers.

Rather, it means the industry must carefully evaluate:

- Where future installation growth still exists

- Which markets continue supporting favorable pricing structures

At the beginning of this year, many Chinese manufacturers had planned to reduce production because:

- Demand was cooling

- Manufacturing costs were increasing

- Profitability remained weak

However, the export tax rebate announcement effectively revived overseas demand.

Manufacturers responded by:

- Increasing production

- Raising price quotations

- Attempting to recover higher manufacturing costs

While domestic Chinese acceptance of these higher prices remains limited, overseas markets have continued procuring aggressively ahead of the policy change.

Importantly, the underlying supply-demand imbalance does not fundamentally change because of the export tax rebate removal.

Europe had already been stockpiling modules in anticipation.

What the policy truly does is establish a new manufacturing cost baseline.

Current DDP module quotations into Europe are now moving above 12 US cents per watt peak.

Once the rebate removal takes effect, manufacturers’ costs will rise approximately another 9%, creating pressure for additional price increases.

The critical question is whether those prices can actually be sustained.

Historically, whenever prices are increased because of policy announcements — without meaningful changes to underlying market fundamentals — prices eventually return toward cost levels.

Therefore, future European module pricing will ultimately depend on:

- Silver prices

- Polysilicon prices

- Manufacturing discipline

- Actual supply-demand dynamics

There is now a new cost floor in the market, and that will define future pricing.

00:29:22

So what are market participants doing in response?

Many companies have already accelerated procurement activity ahead of April.

Transaction prices are now around 11 US cents per watt peak and continue moving upward.

However, after April:

- Procurement activity is likely to slow significantly

- Prices may initially spike

- Downward pressure is likely to return later due to oversupply dynamics

That is essentially our outlook for the European market.

I believe we now have many questions coming in, so perhaps we can move to the Q&A session.

00:30:04 — Q&A Session

Rasa Jakaitis:

Thank you, Marius, for the insightful overview of what is currently driving PV module prices and what we may expect throughout 2026.

We have received many questions, so let us move directly into the Q&A.

00:30:15

Question:

Do you expect any adverse impact on solar cell capacity additions in India due to the surge in silver prices

Marius Mordal Bakke:

The Indian market is heavily policy-driven through mechanisms such as:

- ALMM requirements

- Domestic content requirements

- Local manufacturing incentives

What we have seen in India is a remarkable market acceptance for elevated pricing on domestically compliant products.

This is similar to trends previously observed in the US market.

For example:

- Modules assembled in India using Chinese cells may sell for approximately 15–16 US cents per watt peak.

- Fully Indian-made modules using domestic cells can command prices exceeding 30 US cents per watt peak.

Therefore, I do not believe silver prices will negatively impact Indian solar cell capacity expansion.

However, they will likely increase prices for domestically compliant modules used in Indian projects.

Several leading Indian manufacturers already announced price increases of roughly 25% in January due to rising silver costs.

00:33:01

Question:*

What impact could the EU–India Free Trade Agreement have on India’s solar PV industry in the long term?

Marius Mordal Bakke:*

India has significant manufacturing capacity coming online.

At the same time:

- Domestic installations are growing rapidly.

- Access to the US market may become more difficult due to ADCVD investigations.

If manufacturing capacity grows faster than domestic demand, prices will naturally decline.

However, Indian manufacturing costs are not truly 30 US cents per watt peak. Those costs will eventually need to come down before Indian exports become highly competitive in Europe.

Indian manufacturers may compete particularly well within Europe’s resilience-based procurement frameworks under the Net Zero Industry Act.

However, pricing competitiveness remains essential.

00:34:51

Question:

Is copper replacing silver, and will this happen in the short term?

Marius Mordal Bakke:

Yes.

We have already seen announcements from major manufacturers such as:

- LONGi

- Jinko

- JA Solar

Many are transitioning production lines toward:

- Full copper substitution

- High-copper concentration pastes

This is especially common for back-contact technologies.

Heterojunction manufacturers have already used silver-plated copper for some time because lower processing temperatures make it technically feasible.

We expect significantly more copper-contact solar cells in production during 2026 compared with 2025.

00:36:03

Rasa Jakaitis:

Have manufacturers indicated whether replacing silver with copper could reduce efficiency?

Marius Mordal Bakke:

I do not believe manufacturers openly emphasize efficiency losses, but some trade-offs are implied.

Copper introduces challenges including:

- Increased degradation risk

- Greater sensitivity to humidity

- Lower conductivity compared with silver

Over the lifetime of a module, these factors could impact long-term performance.

00:37:24

Question:

If procurement slows after April 2026, can we assume prices will eventually normalize despite the export tax rebate removal?

Marius Mordal Bakke:

Possibly, yes.

When export tax rebates were reduced from 13% to 9% in December 2024, manufacturers initially absorbed the cost themselves.

However, with manufacturing costs now significantly higher due to:

- Elevated silver prices

- Higher polysilicon costs

manufacturers cannot indefinitely absorb additional losses.

They will attempt to share those costs with buyers.

After 2026, I see two possible scenarios:

1. Prices stabilize slightly above manufacturing costs.

2. Prices behave as they historically have after policy changes — rising temporarily before eventually falling again due to oversupply.

Ultimately, market discipline will determine which outcome prevails.

00:40:42

Question:

Why did silver prices increase so rapidly?

Marius Mordal Bakke:

I am not a silver market analyst, but the explanation appears related to:

- Supply shortages

- Strong demand

- Large quantities of silver being redirected toward the US market

At the same time, silver supply is inherently inflexible because most production is a byproduct of other mining operations.

That combination created an extreme supply-demand imbalance and significant price volatility.

Many analysts believe current silver prices are unsustainably high and may eventually normalize.

00:41:59

Question:

How will the export tax rebate removal affect the battery energy storage system (BESS) market?

Marius Mordal Bakke:

The timeline for BESS differs somewhat.

The industry is experiencing a similar dynamic to what solar experienced previously, but full rebate removal for storage products will occur later.

Importantly:

- The European BESS market is not as oversupplied as solar.

- Demand for storage continues growing rapidly.

- Storage economics remain attractive.

As a result, I am less concerned about BESS profitability than module profitability.

00:43:50

Question:

Could some manufacturers go bankrupt because of the export tax rebate removal?

Marius Mordal Bakke:

Consolidation is already occurring within the Chinese solar industry.

Manufacturers are certainly struggling.

The rebate removal may accelerate consolidation somewhat, particularly among Tier 2 and Tier 3 manufacturers.

However, I do not believe it alone will be the decisive factor.

These companies were already under severe financial pressure.

00:45:46

Question:

Why do costs matter in a market characterized by severe oversupply?

Marius Mordal Bakke:

Because manufacturers have been operating at losses for nearly two years.

If buyers want newly manufactured modules directly from production lines, they will likely need to pay higher prices because production costs have increased.

Older inventory stored in warehouses may still be available at lower prices.

Technology evolution also matters.

Over the last several years, the industry transitioned through:

- Aluminum back surface field

- PERC

- TOPCon

- Heterojunction

- Back-contact technologies

Newer technologies naturally command higher pricing.

00:47:37

Question:

What actions can EPCs, developers, and investors take before April 1st to mitigate these changes?

Marius Mordal Bakke:

The obvious response is to procure ahead of the deadline.

However, whether that makes sense depends on current quotations.

If manufacturers are already pricing modules as though the rebate removal has occurred, waiting may be reasonable.

Ultimately, the decision depends on:

- Project timelines

- Financial modeling

- Procurement strategy

The increase itself — perhaps around 2 US cents per watt peak — does not dramatically alter total project capex.

Prices are likely to continue increasing until April, remain elevated briefly afterward, and then face renewed downward pressure.

00:49:26

Audience Comment:

The export tax rebate removal may not significantly affect overall project economics because a 9% module price increase only translates to approximately 2% of total project capex.

Long-term oversupply could eventually offset these increases.

Marius Mordal Bakke:

I largely agree.

The rebate removal alone will not make or break project economics.

Its main impact has been creating a surge in procurement activity that temporarily allowed manufacturers to raise prices.

00:52:27

Question:*

What factors could counter expectations of declining solar installations in Europe?

Marius Mordal Bakke:

The primary issue is not module pricing — it is project economics.

If electricity prices are negative or capture rates are extremely low, projects struggle financially even if modules are inexpensive.

The key factor that could support continued growth is battery storage.

Pairing solar with four-hour battery systems can dramatically improve capture prices.

In fact, our analysis in Germany showed that hybrid solar-plus-storage systems could achieve capture rates above 100% compared with approximately 56% for standalone solar.

This is why storage is becoming the key growth enabler in mature solar markets.

California provides a good example:

- Roughly 93% of the interconnection queue now consists of solar-plus-storage projects.

- Only about 4% is standalone solar.

That is likely the direction Europe will increasingly move toward.

00:56:16

Question:

Could the Chinese government reconsider the export tax rebate removal due to slowing demand and rising silver prices?

Marius Mordal Bakke:

I do not believe so.

Historically, once Chinese policymakers announce such measures, they generally proceed with implementation.

I fully expect the rebate removal to take effect.

00:56:52 — Closing Remarks

Rasa Jakaitis:

We still have several unanswered questions, but I would like to remain mindful of time.

The volume of questions received today clearly demonstrates how important this topic is for the industry.

Thank you once again, Marius, for such an insightful presentation.

For those questions we were unable to answer live, we will follow up via email.

Before we conclude, I would like to share one final perspective from Sinovoltaics.

Well-structured procurement contracts can help mitigate unexpected PV price increases by clearly allocating risks rather than assuming price stability.

Mechanisms such as:

- Index pricing

- Change-in-law clauses

- Tariff pass-through clauses

- Transparent treatment of freight costs, duties, and foreign exchange exposure

can help transform market volatility into manageable and bankable risks.

While contracts cannot prevent price increases, they can help protect project economics when properly optimized.

Sinovoltaics supports developers, EPCs, and investors in reviewing and optimizing procurement contracts to strengthen cost control and improve risk resilience.

Thank you again to everyone who joined us today.

We will share the webinar recording along with responses to unanswered questions.

Marius, thank you once again for your time and contribution.

00:58:37

Marius Mordal Bakke:

Thank you for having me, and thank you for all the excellent questions.

00:58:45

Rasa Jakaitis:

Thank you everyone. Goodbye.

Visit sinovoltaics.com to learn more.