Europe's battery energy storage system (BESS) market is entering a new phase of growth. As project pipelines expand, competition intensifies, and investment continues to flow into the sector, developers, investors, and asset owners face increasingly complex decisions around market strategy, supplier selection, and long-term project performance.

In this webinar, experts from Wood Mackenzie and Sinovoltaics explore the latest developments shaping Europe's energy storage landscape in 2026. Cecilie Kristiansen, Research Analyst for Energy Storage EMEA at Wood Mackenzie, provides an in-depth market outlook, highlighting the leading developers, emerging regional trends, and the factors driving the next wave of BESS deployment across Europe.

Complementing the market perspective, Tristan Moeller, Business Development Director for Central Europe at Sinovoltaics, shares practical insights into supplier due diligence, financial stability assessment, quality assurance, factory auditing, and risk mitigation strategies for utility-scale BESS projects.

Moderated by Rasa Jakaitis, Media Manager at Sinovoltaics, the discussion also covers audience questions on battery technologies, market business models, cybersecurity considerations, supplier selection, and the future outlook for Europe's rapidly evolving energy storage sector.

Watch the full webinar recording or read the transcript below to gain valuable insights into the opportunities and challenges shaping Europe's BESS market in 2026.

Webinar Transcription:

00:00:00

starting to pick up and that's driven by two key things here. Storage is a dynamic stability that is able to take advantage of its key partnerships pipeline >> which means that we have to really in this case dig deeper now it is really important to do it at the factory that your assets are going to be. >> So hello everyone and welcome to today's webinar. thank you for joining us as we explore one of the fastest moving segments of the European energy transition battery energy storage

00:00:35

systems or as we call them BES. Across Europe storage projects are being developed and built at breakneck pace. Pipelines are expanding competition is intensifying and projects are scaling up in both size and complexity. At the same time, supplying chain decisions are and procurement strategies are becoming more critical than ever. So today's session will give you both a market level view and practical project level perspective on what's happening and what it means for developers, asset owners

00:01:09

and suppliers. So before I introduce you to I before I introduce the two guest speakers let me remind you some basic housekeeping rules. So this webinar will take for about an hour. Two expert presentations will take around 45 minutes and it will be followed by a Q&A session at the end. So during the presentations at any time please use the chat box to submit your questions. the chat box you can find on the right hand side of your screen and please be reminded that this webinar

00:01:45

is being recorded and will be uploaded on Sinovoltaics YouTube channel. So if you want to stay ahead of the curve in terms of renewable energy updates please don't forget to subscribe to our YouTube channel. So now let me invite you on the stage Cecilie Kristiansen a guest speaker. Cecilia. yep. Hi, Cecilia. Good to see you. >> Hi, everyone. Good to see you, too. >> So, Cecilia is a research analyst in Wood Mackenzie's power and renewables team where she focuses on energy storage

00:02:22

markets across Europe, the Middle East, and Africa. She closely tracks market developments, project pipelines, and competitive dynamics across these regions. And prior to concentrating on storage, she worked on solar and onshore wind analysis in the Middle East and Africa, monitoring projects, transactions, and policy developments. Before joining with McKenzie, she also worked as an ESG analyst, advising on sustainability focused investments, bringing a valuable perspective on how finance and clean energy intersect.

00:02:54

Cecilia also holds bachelor's degree degrees in international relations and business administration from IE University in Madrid. So again welcome Cecilie good to have you today. speaker from Sinoalt side. today we have Tristan Moeller my dear colleague. Tristan please come up on the stage. >> Hi Tristan. So Tristan Moellera, he's a business director of Central Europe at Sinovoltaics and Tristan brings deep hands-on expertise in Bass and PB product standards, technical due diligence and

00:03:33

compliance driven risk assessment across global supply chains. In his role, he works closely with manufacturers, developers, and investors to make sure their PVN best projects are their risk and highest quality. So one final thing before I hand over the virtual microphone to Celia, I would like to remind those of you who are seeing the Sinovoltaics webinar for the first time. Just a reminder on what Sinovoltaics does. So Sinovoltaics is a Dutch German company providing technical compliance and quality assurance services for

00:04:10

battery energy storage systems and PV. We offer inspections, factory audits, ESG reporting and traceability audits for utility scale developers and investors. We have on-site teams across the globe. And with over 15 years of experience, we have already audited more than 350 PVN bus factories globally covering all major components such as modules, inverters, transformers, cables, etc. So without further ado now, Cecilia, over to you. Let me help you pull up the presentation. okay. lovely. Thanks so much. H thanksa for

00:04:52

the introduction and also for inviting Wood Mackenzie to be part and to present a bit from our competitive landscape today. H and good afternoon everyone as well. Thanks so much for joining the webinar. As Kasa said, I'm Cecilie Kristiansen, a research analyst covering energy storage in Europe, the Middle East, and Africa at Wood McKenzie. I've been with the team for over two years now and but yeah, so on to the topic of today. So today we're tackling what I think is probably one of the most interesting

00:05:22

questions in the European energy market right now and that is to answer who's actually leading the battery storage boom. The European market has shifted so quickly in the past couple of years and to get a clear oversight of what actually is forming and shaping this market is key. If you've been keeping up with the market over the past couple of years, you probably know that these things are moving incredibly fast. The players who were on top just two years ago aren't necessarily the ones leading

00:05:51

today. So, today we'll take a look at where the market stands, who the big players are, and what's driving these pretty dramatic shifts in the market. But before I get too much into the presentation, I also want to give a quick bit of context on Wood McKenzie before we dive into the data today. So for those of you who are not familiar with us, Wood McKenzie is a research, consulting, and data analytics company. We provide our clients with the latest data analysis and forecasts on different

00:06:20

energy and natural resource markets. And we also advise and consult our clients about their strategic decisions and development plans. And I'll mention this upfront because I think it really matters for what I'm showing you today. The analysis I'm going to be showing is built on Wood Mackenzie's proprietary project database. We track every utility scale storage project we can find across Europe and globally. And when I say that, I mean every project. Our asset tracking team scour announcements,

00:06:48

filings, databases, you name it. They work very hard. But that also means that we're able to be very proud of having a very comprehensive database. Our database is actually so comprehensive that even the European Commission uses it as their official energy storage inventory as part of the JRC. So when I show you who owns what and where projects are, this is really the most complete picture you're going to get. So let's dive a bit further into the presentation. Now I want to give you

00:07:16

guys a lay of the land of what I'm planning on covering. First of all, first we're going to dive into who's actually leading the market. We're going to look at top owners and developers, and you'll see that some names have really been moving around quite a bit here. Secondly, then we're going to look into how they're competing because the strategy the strategy that works in the UK for example is not what's going to work in Italy or Poland. And here we really see that regional differences

00:07:40

really matter. And finally, I want to talk and discuss openly with you guys what's coming next as well. About 70% of the storage pipeline that we're going to be looking at today is still in the early stage of announcement or early development. So there's a lot left to play for here. We'll talk about what separates the companies that can actually deliver from the ones that will remain in the pipeline for a long time. So, let's get into it. So, 2025 was a big year for Europe and

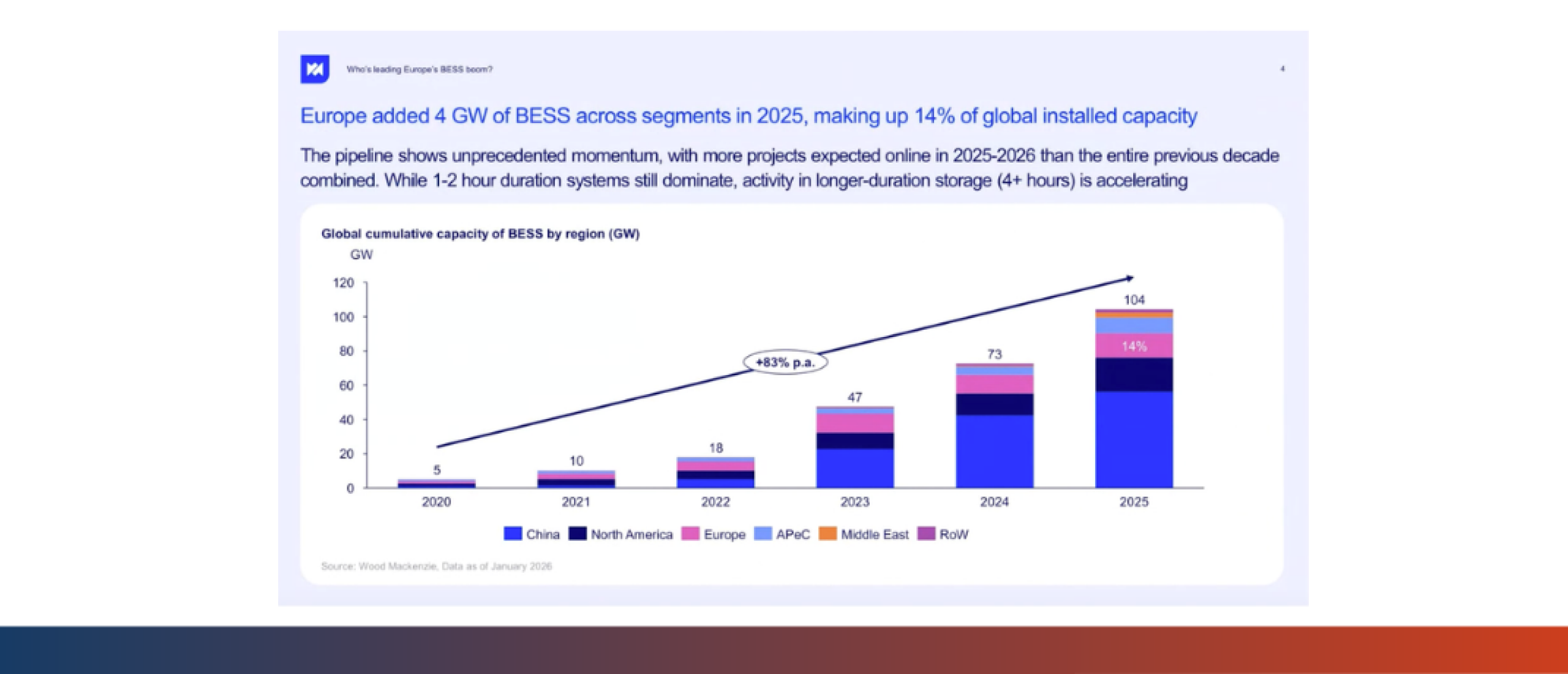

00:08:10

battery storage. Europe added 4 GW of battery storage across all segments. That made up about 14% of global installed capacity, which is substantial. If you look at this chart here for a second, we've got more projects expected to come online in 2025 to 2026 than came online in the entire previous decade. So, we're really seeing monumental growth across the industry. Furthermore, in currently in terms of battery storage sizing trends, we can still see that 1 to2 hour systems are dominating, but longer duration

00:08:44

projects, namely 4 plus hours, are really starting to pick up. And that's driven by two key things here. Grids needing more sustm or variable renewable energy that we're seeing come online and that desperately needs to be balanced. The 83% year-on-year growth here that you can see over the past 5 years tells you that storage isn't experimental anymore. This is the infrastructure that's being built of the future of our future energy grid coming online. So, this is probably one of my favorite

00:09:20

ways to visualize actually what's happening in the energy storage market currently. What you can see on the screen right now is a plot chart of all of the operational projects that Wood Mackenzie has tracked in Europe. Each bubble here is a project. The size is the capacity and they're plotted both by duration and when they've come online. So, first thing that I want to highlight for you guys here, look at 25 and 2026. There's just a massive class cluster of projects that are getting bigger and

00:09:48

bigger and a lot of them are in that two to four hour duration sweet spot that I currently me recent that I just mentioned. Excuse me. which makes a lot of sense because that's where you can play in both merchant markets and capacity auctions. Second thing you see those bubbles that are stretching out towards the top of the graph those are longer duration systems. projects are getting bigger and le and with bigger duration as well, which tells you that the market's maturing beyond just

00:10:14

short-term arbitrage into more complex grid services. And this is all pulled from our Wood Mackenzie database. We're currently tracking over 3,000 projects across 37 countries in Europe alone. And that doesn't even take into consideration our full global coverage. And this covers everything from operational to maybe this happens someday. the what woodmck we do use our own proprietary perspective and an analytical take to make sure that we're filtering in and only including projects that we believe have some likelihood of

00:10:45

coming online to not include everything because there can be as many know there's a lot of different projects that are announced that often don't materialize. It's a lot of data but it gives us a really clear view of where the market is headed. So, let's then try to ask the question, who's actually leading in the market? And here's where it gets quite interesting. The top 15 asset owners in Europe now control 43% of operational capacity. So, that's a pretty concentrated market that

00:11:14

we're looking at here. It's increased around 7% since last year also. But what I want to especially highlight here is look who's number one. It's Enel. Enel just overtook Gresham House. And this is a big deal because Enel is the first utility since Woodmax started tracking the competitive landscape to hold the top spot. They've got about 1.7 gawatts operational of projects with an average duration around 4 hours. Gresham House on the other hand has roughly one point a little over a gigawatt of energy

00:11:45

storage projects online with an average with a 2hour average duration. So what does this really tell us about the markets? But we can see here that capital is getting more concentrated. The biggest players, especially utilities with balance sheets and existing grid relations, are taking more market share. Also, Enel's portfolio is almost entirely in southern Europe, which I thought was important to highlight, mostly in Italy, as many are probably aware. And that's a big shift that we're seeing from the UK heavy

00:12:13

portfolios that have really dominated the top rankings in the past couple of years. It's a signal that Italy's capacity market and auction mechanisms are really working. And it's also a signal of a developing and maturing market across all of Europe where the UK slowly, though still remains dominant, but slowly starts to see competition from other areas across the continent. Now, let's also take a look here at the company type breakdown on the right. We've got utilities in orange

00:12:39

that are taking a bigger slice of the pie since last year. investment funds are decreasing their market share and IPs and IFPS namely independent flexibility providers are starting to show up are really starting to show up as a key player in the market in terms of where the storage pipeline is at in the project development. You can see here all the way on the right hand side of things that 71% of all projects are still in the announced stage, 15% are under construction and only 14% are operational. So here

00:13:12

execution matters and here's something that I think is really important to kind of explain and highlight a bit better how this market is actually changing here. A lot of these companies that you've seen on the previous slide and that we hear talk a lot of talk about in the storage environment for example Zenob, Fedra, Elsmi, Intergen and Statera. They're backed by massive institutional investors. So that's the names of KKR, EIG, CIP, Seven Global Investments, and many more. So the market is changing

00:13:47

now. These aren't startups that are scrambling for project financing. They're portfolios backed by billions in institutional capital. And what that means is that they can secure debt financing, move fast, absorb risk, and really build at scale. And I think the perfect example to highlight this is Future Energy. They entered the market in 2024 and immediately they announced the largest battery project in Europe at almost at 1.5 gawatt in the UK. Now that you don't do that without serious financial muscle

00:14:20

behind you and it's showing how this financial backing that many companies are starting to feature are really pushing forth the new wave of storage projects that were starting to come are starting to come online. This is really a completely different game than five years ago when it was a bunch of independent developers chasing subsidies. And I think we can further see this here. Yeah. and we see this trend even clearer when we look at the biggest projects in the continent. These are the

00:14:48

top 20 biggest projects in the European pipeline right now. So the first thing you'll notice here is nine out of the top 10 projects are in the UK. And honestly, that makes a lot of sense. The UK just has the most mature market. They have the clearest revenue stack, the strongest grid infrastructure for storage to come into play and the most liquidity in terms of financial players as well. If you want to build something massive, the UK has been the place to do it. But this is changing. What you can

00:15:18

see on the graph here is we're also seeing Belgium, Switzerland, and Germany, and Germany showing up in the top 20. And these aren't small projects either. Many are from 600 megawatts to over a gigawatt. These are power plant scale assets that are really starting to shape the new generation of storage that's coming online. So now I want to move forward and talk a bit about this regional overview as well because as we all know Europe isn't just one market. It's a bunch of different

00:15:48

regulatory regimes, grid operators and revenue models. And understanding how companies compete regional is therefore critical to understanding how storage is being deployed across Europe. This chart on the right hand here shows something that surprised me when I first saw it. You'd expect collocation to be highest in the least mature markets, right? It's what we've typically seen. storage paired with renewables because standalone revenue either wasn't proven yet or hasn't or the market

00:16:20

mechanisms aren't there for standalone revenues to come through. But that's not necessarily what's happening in all of our markets. We see here that southern Europe has the highest share of hybrid projects at 30%. Despite being one of the faster maturing markets with namely Italy included in it, but also Spain that has a lot of buzz around it these days. Northern, Western, and Eastern Europe are much more overwhelmingly focused on or developing standalone projects. So, it's a question

00:16:49

I posed myself. What's going on in Southern Europe here? And here, it's actually a permitting story, which isn't something that's unique to Southern Europe as we've seen it in other countries as well, but especially in Italy and Spain. Collocating storage with renewables has really been a help to get through permitting faster. You're not necessarily asking for new grid connections depending on your configuration of course of your battery to your solar project but you're

00:17:15

rather upgrading existing renewable sites. So, it's become a strategic choice, not necessarily a sign of market immaturity, and has been especially beneficial in countries like in southern Europe, like Spain, for example, that have been so quick in developing and deploying out solar fleets, but are now struggling with the project economics of solar only sites. That being said though, we are seeing southern Europe mature rapidly, especially when we take a look at Italy's Italy's maxi auctions and recent

00:17:45

auctions in recent tenders in Spain as well, which are specifically driving standalone deployment by creating bankable capacity market revenues or substantial subsidies. Finally, here Eastern Europe being 80% standalone is quite interesting as well. That's developers making a bet that merchant and capacity markets will develop as we're starting to see them come through even though they're not fully there yet. It's a riskier play than collocation, but the upside is bigger if those markets materialize.

00:18:18

So, what's the takeaway here? Collocation isn't always about market maturity. Sometimes it's a smarter way to navigate local constraints. Southern Europe is a show here of how strategic hybridization can lay the path for sophisticated storage specific policy to follow suit. So then if we go into talking a bit about who are the top regional asset owners, what this slide really shows is that there's no winning strategy across Europe. You need to adapt to your local conditions. Western Europe is largely utility and

00:18:52

IFP territory. RDWE wins because they have scale, existing grid relationships, and the balance sheet to move fast. While Giga Storage is a dynamic IFP that is able to take advantage of its key partnerships to execute its pipeline in Germany, execution matters more than just innovation. If you can build big and build fast, you can really win through here. In Northern Europe, especially in the UK, rewards it's really rewarding financial sophistication. sophistic sophistication, sorry. Innova,

00:19:25

Fedra, and Gresham House, they're not utilities. They're financial operators and IFPS who have figured out how to stack revenues. Furthermore, capacity auctions, merchant trading, and frequency response they're playing. So, these players are playing a complex game and they're getting good at it as well. Finally, Southern Europe is policydriven and therefore favors local champions. NL isn't just the biggest in the region. They're Italy's national utility. So, they understand how Max's

00:19:56

auctions work. They can navigate permitting and they have government relationships. In markets where policy creates the revenue, being an insider is really a huge advantage. And last of all, Eastern Europe is still anyone's game. We see Greenbolt, our power, and PGE are placing bets on markets that don't fully exist yet. Poland, Bulgaria, and Romania. While they have massive pipelines, almost nothing is operational. Though I will say that is very quickly changing as we're seeing in the case of Bulgaria

00:20:27

especially. The winners here will be whoever figures out grid connections and permitting first because right now those are the bottlenecks. So the key takeaway here is market mature markets favor execution at scale while policy-led markets favor local incumbents and early stage markets favor whoever can get can navigate infrastructure constraints. The UK seems to be the only place where you can win on pure financial engineering for now though that though that will surely start to change as we see offtake contracts grow across the

00:21:00

continent. So I want to finish off by asking a bit what's next and really posing three big questions going forward. The first question is about capital access. Can mid-tier developers survive without institutional backing. We've seen how much capital matters now. It enables scale, speed, and absorbing risk. If financing gets tighter, we expect a lot of small players are going to struggle. Secondly, project scale. Are these 100 megawatt plus projects becoming the standard? We're seeing that in the UK

00:21:35

and it's is spreading to continental Europe as well. Bigger projects can mean better economics, but they also mean more complexity, permitting, grid connections, and the need for offtake. Not every market is ready for gigawatt scale storage yet. And finally, regional diversification. Which emerging markets will actually deliver? Poland, Spain, Romania, they have big pipeline numbers. But pipelines don't mean anything if you can't actually build them. So permitting, grid bottlenecks, and unclear revenue models,

00:22:06

these are the real risks that we're seeing. The markets that figure out how to move fast will be the ones that are able to access capital as well. With 70% of the storage pipeline still at an early stage, execution is everything. That's what's really going to separate leaders from everyone else. So to wrap up, Europe's battery market isn't experimental anymore. I think we've really been able to see that throughout the presentation. It's infrastructure. The players leading

00:22:33

today have scale, capital, and most importantly, they can actually execute. Utilities like Enel are really taking share from financial players as they take a step back and institutional backers focus on enabling newcomers like Fedra to jump straight into the lead. Now, the UK is still our gold standard, don't get me wrong, but Southern Europe is catching up thanks to better policy. And honestly, Eastern Europe could be the next frontier, but it's still too early days to see that. So, thank you so

00:23:00

much for your time. And I pass it back to Rasa. >> Thanks a lot, Cecilia. Thank you for yeah, this very detailed and interesting overview of who's leading the best game in Europe in 2026. let me invite now Tristan back on the stage who will go deeper into the practical side of the best race given that some markets are still maturing and as Celia said we still need to figure out the rules of the game. So if you are in this game it's very important that you know how to

00:23:40

select the right supplier and I think we didn't touch upon the suppliers just yet. So Tristan over to you. Can you see your presentation? >> no, not yet. >> Let me just pull it up real quick and I will be leaving this stage real soon. Can you see it? Okay. >> yeah. Yeah, more or less. The ratio doesn't doesn't work 100%. Now you're gone. Hello brother. >> Okay, I am back. >> Life is a box of chocolate. >> apologies. also webinar

00:24:29

attendees the webinar platform is playing some tricks with us today. So let me once again share the presentation and I will remain on the screen with you Tristan if you don't mind. I don't think that is disadvantaged. Thank you so much Raza for the introduction. Thank you so much Cecilia for your presentation part. It is really interesting to see how the market is developing in different parts of Europe and in the UK and who are the big players and who are the

00:25:00

the big investment groups that are powering those projects. Speaking of investment groups and speaking of the landscape of battery storage suppliers at large, things that is things that are getting more and more clearer is that battery storage projects even though they are happening on European soil or on UK soil are more intertwined now with each other. we have seen European players, American investment groups, we have seen UK based companies and one of the things that are that is getting more and more

00:25:35

complicated in this u geopolitical kind of situation is to really understand who the supplier of your battery storage system is actually. So in order to really make the ownership of the companies transparent as somehow possible, there are ways to vet the companies and to basically scan where and how they are functioning at each and every stage. One of the maj one of the advantages in doing that is that not only will you gain information about those companies in terms of factory locations which is a little bit more

00:26:12

onhand information but you will also understand how the supply chain is being built up by those companies allowing you to improve the transparency of the supply chain at any given time. We at Sino takes we can help you with doing that. if you don't want to spend your time doing that yourself during the tender process or the RFP process or while you're just vetting the suppliers that you are thinking of working together with or that you are short listing at this point in time.

00:26:53

Another thing that we here do at Cyovics, my mother used to say there is nothing better than something that is cheap. I would argue there is things that are even better if they are for free. which is one of those things here. we provide you with a financial stability ranking in a very reoccurring phase. So what we do is we periodically send these out or we publish them which allows our clients but everybody actually who is interested in doing that to have a peak at the financial stability of battery storage

00:27:30

companies. Now I would like to dig deeper a little bit into that because in order to raise those utility scale projects that Cecilia were was talking about. I think it is really important to understand which company is able to keep the base to scale those projects to the sizes that we've seen. I mean we have to put it into perspective. When I was working or started to work in battery storage a 5 megawatt hour or 10 megawatt hour project was looked at as quite large. We're talking about 00:28:01

tfold 100fundfold projects now which means that we have to really look and dig deeper now and take the vetting and the scanning of the suppliers more seriously than ever. how we are doing this? So what we do is we use the ultimate zcoring. people that know our company or have been in touch with us for PV modules or inverters know this scoring system already and we have provided this few of those stability rankings along the way for battery storage systems in the past. and the admin zcoring is a bankruptcy

00:28:38

risk model which has been developed in the 1960s. the major markers that are being used for this scoring system is liquidity, profitability, leverage and efficiency. And this is put into a weight formula. I'm very welcoming you to ask for the formula. I mean you can Google it now if you haven't done it by now how the formula looks like. And by the end of the by the end of the formula you will receive a scoring system or a classification of the supplier which is the definition in the

00:29:11

alman scoring system is that everything above 2.99 points is regarded as a low risk of bankruptcy within a time frame of two years. the gray area is between 1.81 and 2.99 which is a neutral zone. so in a sense it goes can go either way. 1.18 is regarded as a high risk or a red zone distress or a red distress zone meaning that there is quite a probability for that particular manufacturing company to have issues financial issues with and bankruptcy looming. where is this being used typically and

00:29:58

and maybe CC knows this admin scoring system as well or heard about it but it's typically used in the credit and counterparty screening. It's a kind of a quick and dirty way to assess the financial situation of a company. Of course, as with every model, there is some limitations which I would like to mention here as well. one backlash is that it is working on historical data. which means that we can only use information that has already been published in the past. So it's not a

00:30:29

forwardlooking but it's looking at the historically data that has been provided through the last years. and also the second one which is more a limitation of our ranking report is that we only use publicly available publicly traded companies. So if you are a developer, IP or an asset owner that is looking out for a certain company then you might not be able to find it within these means because they are not publicly but privately held. Thank you. So this is how the graph then looks

00:31:08

like. So again, for those that know this graph, just as a short description here, I've picked a few suppliers in the in the green zone, which is displayed as the as the as the safe zone, a few suppliers in the gray area, and some suppliers in the red area. I think this graph number one which is then in the in the stability ranking report is the one that is most useful because it really clearly and quickly kind of defines on where the company stands from perspective on of admin zcoring.

00:31:43

Thank you. Another way to assess the stability or the situation of the companies and again I would like to circle back to the point that with growing project sizes the due diligence of selecting a valid supplier is growing is to audit them. Well, this sounds quite simple in the first moment, but the reality shows that there is a lot of ways to get to Rome in this case. An audit can be in different shape or forms. it can also be really relevant if you're looking into ESG and traceability if that is one

00:32:22

of the visions or company u culture things within the investor stock or within the investor circle that ESG and traceability is a must then this is also something which we see time and time again that it is being a request that is being basically passed down to the suppliers what do they Actually in this case you are looking at the quality audits to ensure compliance with the spec specifications and the manufacturing standards. but it what is also really important to know is if you

00:32:58

are conducting an audit if you are doing it yourself if you are hiring someone doing it whatever your weapon of choice is actually in this case it is really important to do it at the factory that your assets are going to build be built in. what we see sometimes is that there is a little bit of pivot going on saying that it is transferable from one factory to the other one which is not the case. We see large differences when it comes to factory quality even within the same supplier.

00:33:31

So auditing one factory and building it another one is not really the choice of options that I would go in this case. something that is really important to notice now that everybody has seen the numbers for the pipelines in the next couple of months and years coming up. in large scale projects and I would assume that all the projects that Cecil has shown us are large scale in my book it can happen that there is a multiffactory approach by the supplier or at least is being pitched by

00:34:04

them. I would recommend in that case to audit all of them just to make sure that the standards are the same across the board for all the factories that are being used for the production of the assets. maybe a little bit of a sales pitch from my end here. But what we also do at COVID is to support an every client factory tour. If you're interested in doing that, please reach out. It's not an issue at all to do that. on the other hand what is more important to understand is that

00:34:34

these days hybrid tours are the choice of most of our clients. What that means is to go there by yourself as a as a client and have an auditor from us as well included in that in that trip to the supplier and do a due diligence while being at the factory yourself. Also something that is really important to notice and which is the wind of the of the of the game right now is that the due diligence required by most of our clients are getting more and more deeper. So we climb up the value

00:35:08

chain and the and the supply chain actually of the of the battery storage suppliers and a lot of the projects are also asking for cell level quality audits at the factories which as most of you can imagine is quite a tricky thing to negotiate with the suppliers because that is where most of the IP lays within producing the cells. Thank you so much. another thing that I would like to highlight here is that production monitoring for those large scale projects will be coming I'm

00:35:46

pretty sure about that it's going to become the norm in determining the quality of the projects and the quality of the assets that are being built. the quality execution is really important now and we are speaking of experience within PV module production and we are certain that this is going to be the way for the bankability for projects in the future for battery storage as well. Those large projects are very cost intensive and high investment is being made in

00:36:20

those projects. So making sure that the assets by the time that they arrive on site is going to be one of the key priorities. and why it is really important is to understand is that at one point in time the QA and QC so the quality of the assets will really differentiate the suppliers on the market. I think it already does. one of the first things that companies are looking at is how well suppliers are prepared to really deliver the quality products to site in order to not have any downtimes.

00:36:59

Meaning that your assets are in a perfect world are always on and you don't have any downtimes that you don't want to have you actually want to use your assets to the maximum capabilities somehow possible. yes, thank you. Yes, thank you so much for your time. and yeah, I think the Q&A session can be kicked off. Raza, I hand you the keys. >> Thank you, Tristan. thanks a lot. And Cecilia, we would like to welcome you on the stage for the Q&A session. also Tristan while you

00:37:42

were you know wrapping up your part about the best supplier selection for the past couple of days I attended solar quality summit in Barcelona and one speaker there said something really wise how to distinguish a good best manufacturer from a bad one. So a good one will promise you many things but it will also add these things to your contract. So I think that's also very essential that you know manufacturers can say a lot of things but it's the most important thing is what ends up written

00:38:14

in the contract. So we have we have a number of questions. Thank you to our audience. let's start with the first question. to you Cecilie so you mention you mostly talked about the developers. Could you elaborate on the on the technologies? So, could you tell us which technologies are the most widespread on the market? >> for sure. I mean, I think it's it's of course not a topic to be avoided, but I think nowadays it's not the most exciting topic to be quite

00:38:48

honest because it is a lithium game by far. A lithium ion battery game is the name of the game these days. There is a divide a slight divide between an LFP versus an NMC. I think at Wood Mackenzie we estimate about a 80/20 split of the market share between them giving maybe a final percent towards sodium ion batteries which are starting to come more into play here but still remain in from our perspective in the long term but for now it's lithium ion batteries great thank you Celia another one for

00:39:20

you from Randall does wood mckenzie have the same type of research for the North American market or any other regions of the world. Is it available on your website? >> We do actually. So for storage specifically, our North American team exactly have a very similar version of this competitive landscape focusing on the American markets. and then also I don't know if your interest is in other terms of technology as well, but I know our solar team also puts out a similar competitive market landscape and that

00:39:51

can be found on our website or you can reach out to me and I can also put you in touch with the with the correct people that can connect you. Good. thank you. Thank you, Celia. question from Andreas to Tristan. Do you have any information on the after sales service of the providers? >> yes and no. we do have that, but we it's not some of the services that we provide in there. No it's not we you we hear a little bit here and there but it's not one of it's not part

00:40:24

of the services which we provide as senov tes if you if you're interested we can have a talk about it separately you can get in touch with me through the contact email it's not an issue at all >> great another one for you Tristan from what are the reasons for the standards to arrive by site within one company shouldn't certification prevent is >> that's a good question. and the reason behind it is that in some cases the supplier of so the person that

00:40:56

you're talking to is not the person that is assembling the battery stoages. So it might be the case that there are several OEMs putting together the assets and as you can imagine it's already really tough to keep the QAQC level within your own company but to spread it over to other suppliers it's even harder to doing that. so that's the reason why different levels of quality exist. You're 100% right. The certifications should be the same but that doesn't really mean that they

00:41:25

are going to be executed the way they should be in some cases. So I hope this answers your question. >> Thank you Tristan. one for Cecilia from PA. based on what's happening in the US regarding the blocking of Chinese manufactured components, do you expect CL EV and the rest to push price competition in Europe? >> I think it's definitely a very reasonable it's a good question. I think it's a very reasonable assumption to have as well. We're definitely seeing

00:42:03

there's a big push in general from Chinese manufacturers to penetrate better through into the European markets and also to work on bringing local production into Europe as well. So, we're definitely seeing a move in that direction and how the US and its protectionism is changing and modifying the market in a way that we haven't expected to see it from beforehand. U another one on the on the price side for you Cecilie from Atul in 2026 will price of battery will reduce what

00:42:46

does the research say on that? >> I mean I don't want to give away too much either because you can definitely get in touch with us and we have some very strong pricing forecasts that are built on very strong assumptions. So I would ask for you to get in touch with us and I would love to share with our supply chain team especially the insights that we have. I know there's a lot of debate and a lot of hot topic now on how lithium specific pricing is affecting the battery pricing going

00:43:13

forward both in the short term and then it through into the long term as well in the short term. We do think that while there are expectations that lithium pricing will go up that the battery price will remain stable and continue to go in an downwards trend. But further than that, I hope you get in touch and then we can talk much more in depth about it. >> Good. another one for you Cecilie from Somia. so do you see an impact of cyber resilience act on supplier selection Chinese versus EU US-based and

00:43:46

maybe Tristan also you can you can comment on that. >> yeah, it's a great question. I so far it's not something that has made a huge impact but this cyber awareness is something that's very much on the tip of many players tongues. So it's definitely something we're seeing coming more and more towards front of mind as well and I think we will start to see it very much in the forefront of people's decisions going forward. But of course it's price is always a matter as well. So, we're going

00:44:19

to see. It'll be interesting to see how those two balance against each other. >> I can just confirm what Cecilia has said here. it's it's something that is kind of looming. I have the feeling that everybody is kind of talking about it in a sense that yeah, something is going to go down, but it's not something that has pushed through in a sense that the selection is now very critical over it. except for some suppliers that might be how should I put this challenging to the

00:44:50

to the current system. So some suppliers as most of our listeners will know are blacklisted for several reasons. >> Okay, thank you both. from Sylvia question to you Cecilia. that's a long one. Though given the exponential growth of grids scale best installations probably also the competition to gain long-term contracts will become tougher in the next years. Do you think that business models for best relying only on services provision will be financially feasible? no I think I think you're very it's a

00:45:31

very good question. I think you're on the money with that as well. Of course, being able to secure any sort of offtake contract and therefore being able to give your investors or your financeers some sort of stronger confidence in what you're putting online, what you're develop or what you're building as a project is very important now. But as markets start to saturate, as time goes on, in general for batteries, the most competitive way to go forward is having this beautiful revenue stack with playing in several

00:45:59

different markets of being able to combine your revenues as the a as different markets saturate across as well. so I think it's going to be very important, very dynamic for batteries to be very active. There's a lot of talk and a lot of consideration of optimization contracts nowadays as well and seeing how batteries can best play in the market. So I think we're going to see it's a it's an emerging topic this year and I think it's really going to be a leading topic in the years

00:46:23

going forward. >> You're on mute. >> Apologies. thank you Cecilia for answering the question. I have another one for you. what business models are majorly adopted in Europe? How do you see this? >> I mean, it's it's what I tried to highlight in my presentation as well when we did the regional breakdown. It's hard to talk about Europe as one place because it's so dependent on your local grid, on your local energy mix, on the different market opportunities you have

00:47:03

in terms of what market mechanisms exist, what regulation is put into play. I can give you an overall view of like business models in terms of I mean it's it's different ways to consider it. Are you we talking business models in terms of how the storage developers are coming into play or business models in terms of how you're financing and bringing revenue into your batteries as well. On the revenue side of things, we're really seeing that depending on the market, a balance between capacity

00:47:31

markets, energy trading, ancillary services, balancing market markets, and now the new theme of inertia markets as well are being combined together to create a revenue stack. And then in terms of business models on who's developing and building the project and how they're financing that, the really emerging trend we're seeing right now is what I highlighted in the presentation as well, which is these big IFPS and IPs that are funded by huge financial investors that are really giving them

00:47:58

the financial and economic backbone to be able to pull through debt financing and even assetbacked financing to be able to really bring online huge projects. Okay, thank you for such elaborate answer, Cecilia. I see that we cover covered all questions. unless there are any other like the last words you want to make Tristan or Cecilia, I would say that we can wrap up today's session. >> Cecilia, maybe you first if you want to if you want to say something. >> Oh, great. Thank you. Yes. well, it's

00:48:39

been it's been great chatting with everyone. I think it's a really interesting topic. We've been putting out this competitive market analysis now for a couple years at Wood McKenzie and it's really interesting to see how such a young market that storage is, how quickly it's developing and how it's maturing at different rates across different countries as well. So very happy to have had the opportunity from CN Voltics to be able to present here. always happy to chat with you guys and

00:49:06

hear much of the expertise that you're able to bring from the supply chain and the supplier side as well. And for anyone that's left with more questions about what we've talked about today or about what Wood McKenzie can offer and can complement your business with as well, please feel free to reach out. Happy to connect with anyone and to keep the conversation going. >> Well, from my side, thank you so much for everything. it was really I learned a lot. Thank you so much. I

00:49:33

didn't promise too much on LinkedIn. it was really nice presentation listening in learned a lot of stuff. So that's I guess the reason joining such webinars. yeah and if there's any question left or if anything that is unclear please reach out to either Cecil or to me or to Raza and we will take it from there. Thank you so much for joining >> and from my end thank you Cecilia for being with us today. Thank you Tristan for your expertise and just a reminder

00:50:05

to the audience that we will share the webinar recording with you in the coming days. so yeah thank you for attending for thank you for the questions and see you in the next webinar series with Sinovoltaics. Bye >> bye. >> Thank you so much. Bye. >> Visit sinovtaics.com to learn more.

Follow us to receive the latest news!

Follow us to receive the latest news!

<:optin-form-placeholder>

Who's Leading Europe's BESS Boom? Market Outlook and Competitive Landscape in 2026

Place comment